.

U.S. consumers in aggregate remained financially healthy entering 2024. That’s the conclusion of new research, which highlights wealth effects, accumulated savings, and normalising credit usage as sources of strength. Our findings suggest that if consumers don’t stoke continued U.S. economic growth, they will at least mitigate downward pressure in the event of a U.S. recession.

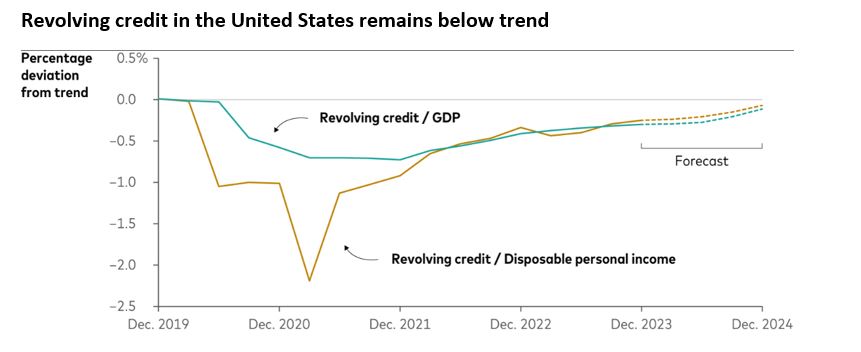

Among the key findings of the research, led by Bob Behal of our Fixed Income Group and Josh Hirt of our Investment Strategy Group: real estate values have driven atypical wealth gains across income distributions since the onset of the COVID-19 pandemic, and distress in lending markets is largely confined to the least creditworthy borrowers who drive the least amount of spending.

Sources: calculations using data as of December 31, 2023, from the Federal Reserve Bank of New York and Equifax.

The chart above shows that, as a proportion of both gross domestic product (GDP) and disposable personal income, revolving credit such as credit card debt and home equity loans remains below its pre-pandemic trend and is likely to normalise only in the fourth quarter of 2024. The likely upshot? More room to run for the U.S. consumer.

Vanguard’s outlook for financial markets

Our 10-year annualised nominal return and volatility forecasts are shown below. Equity returns reflect a range of 2 percentage points around the 50th percentile of the distribution of probable outcomes. Fixed income returns reflect a 1-point range around the 50th percentile. More extreme returns are possible.

Notes: These probabilistic return assumptions depend on current market conditions and, as such, may change over time.

Source: Investment Strategy Group as at 14 February 2024.

Leading indicators suggest that resilient but subdued economic conditions will prevail early in 2024, with a gradual acceleration in the first half supported by rising real household incomes, a reflating housing market, and firming business investment.

Recent growth and labour market data suggest the U.S. economy remains robust as debate continues over the timing of potential cuts in the Federal Reserve’s target for short-term interest rates. Inflation continues to ebb, but remains alert to risks posed by still-strong wage growth.

High-frequency housing and auto sales data as well as data from purchasing managers’ indexes suggest that weak economic growth has carried into the new year. As a structural property downturn drags on the economy, private demand and business confidence remain subdued. The government has responded with broad but incremental stimulus measures, including support for the ailing housing and equity markets.

We believe the Governing Council of the European Central Bank (ECB) will look to first-quarter inflation and wage data, the latter of which will be available only in late spring, to confirm that it can sustainably return inflation to the ECB’s 2% target. That would allow the ECB to initiate a rate-cutting cycle with its June 6 policy announcement, with 25-basis-point cuts potentially at each of its final five policy meetings of the year.

The U.K. economy may have fallen into a technical recession, marked by two consecutive quarters of declining activity, in the second half of 2023. But high-frequency indicators suggest that a modest return to growth, around 0.1%–0.3%, may be underway in the first quarter.

Emerging-market central banks were ahead of their developed-market counterparts in raising policy interest rates during the latest hiking cycle. Now, with inflation slowing, interest rates becoming more restrictive, and growth concerns rising, emerging-market central banks are leading the cutting cycle. Examples of banks that have lowered their policy rates include Banco Central do Brasil, Banco Central de Chile, and the Czech National Bank.

Canada’s economy contracted in the third quarter compared with the second, but it avoided falling into a technical recession because second-quarter economic activity was revised from negative to positive.

IMPORTANT: The projections and other information generated by the Vanguard Capital Markets Model® regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time.

The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model is a proprietary financial simulation tool developed and maintained by Vanguard’s primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include U.S. and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, U.S. money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

This article contains certain 'forward looking' statements. Forward looking statements, opinions and estimates provided in this article are based on assumptions and contingencies which are subject to change without notice, as are statements about market and industry trends, which are based on interpretations of current market conditions. Forward-looking statements including projections, indications or guidance on future earnings or financial position and estimates are provided as a general guide only and should not be relied upon as an indication or guarantee of future performance. There can be no assurance that actual outcomes will not differ materially from these statements. To the full extent permitted by law, Vanguard Investments Australia Ltd (ABN 72 072 881 086 AFSL 227263) and its directors, officers, employees, advisers, agents and intermediaries disclaim any obligation or undertaking to release any updates or revisions to the information to reflect any change in expectations or assumptions.

February 2024

Vanguard

vanguard.com.au

Hot Issues

January - March 2024 archive