Investment and economic outlook, August 2023

Read our latest forecasts for investment returns and our region-by-region economic outlook.

.

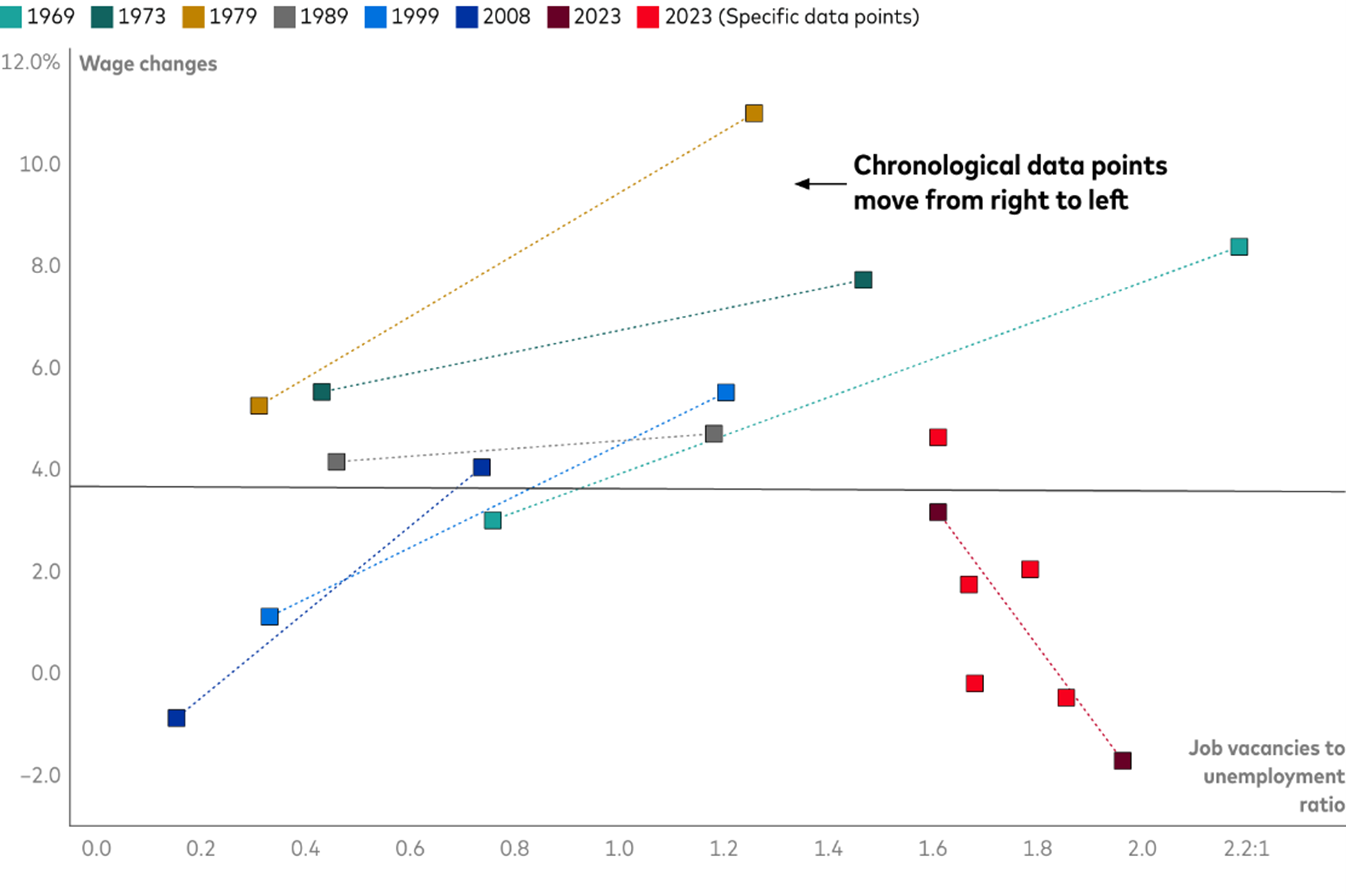

A funny thing has happened in the United States labour market since the ratio of job vacancies to unemployment (V/U) started to fall early this year: The pace of monthly wage growth has accelerated. Typically, a declining V/U—a sign of labour market softening—is accompanied by slowing wage growth.

Intuitively, wage growth should ease as demand for workers falls. That it hasn’t is a function of lingering post-COVID-19 dynamics, said Adam Schickling, a Vanguard economist who studies the U.S. labour market.

“There are two key reasons for this phenomenon,” Schickling said. “Sectors remain where demand for labour well exceeds supply, such as health care, professional services, and leisure and hospitality. And firms have been reluctant to fire or lay off workers given the challenging labour supply environment.” Schickling also noted that real (after-inflation) unit labour costs are below pre-COVID-19 levels for many sectors, providing room for wages to rise further without immediately spurring inflation.

A softer labour market … and rising wages

Notes: Wage changes are nominal and measured on a monthly seasonally adjusted annualised basis. Years depicted reflect periods of labour market softening as measured by a declining ratio of job vacancies to unemployment. A ratio of 1:1 suggests a labour market in balance. The ratio as of May 31, 2023, was 1.6:1. The data representation for 2023 includes actual data and the trend line. Data representations for past years include only trend lines to aid readability.

Sources: Vanguard analysis of data from the U.S. Bureau of Labour Statistics and Refinitiv Datastream through May 31, 2023.

The findings are part of the backdrop for changes to Vanguard’s U.S. economic and monetary policy forecasts. As more workers find jobs and earn more, better-positioned consumers will support growth, pricing power, and interest rates.

The views below are those of the global economics and markets team of Vanguard Investment Strategy Group as of August 16, 2023.

Region-by-region outlook

Australia

While markets price in just a 60% probability of a rate hike by the end of the year, Vanguard forecasts one or two more policy interest rate increases to around 4.35%–4.6%. While there have been signs of some deceleration in consumer price increases, “the Reserve Bank of Australia will want to hike one or two more times to put a final nail in the inflation coffin,” said Alexis Gray, a Vanguard senior economist.

- Headline inflation, as measured by the Consumer Price Index, declined from 7.0% year-on-year in the first quarter to 6.0% in the second quarter. We expect headline inflation to fall to around 4.5% by the end of 2023, as higher interest rates dampen demand, and for it to reach the RBA’s target band of 2%–3% by late 2024 or 2025.

- GDP grew by a less-than-expected 0.2% on a seasonally adjusted basis in the first quarter of 2023 compared with the fourth quarter of 2022. Compared with a year earlier, it was up by 2.3%. We continue to expect GDP growth of 1%–1.5% for all of 2023, though risks skew to the downside. Our proprietary leading indicators model suggests that growth will remain below trend in the coming quarters amid weak consumer confidence and subdued consumption. We assign about a 40% probability of recession over the next 12 months.

- The unemployment rate held steady at 3.5% in June, as the employment-to-population ratio remained at a record high of 64.5%. We expect the unemployment rate to rise gradually this year to around 4% as financial conditions tighten and to continue to rise in 2024.

United States

Amid continued resilience in the labour market and the broader economy, we’ve revised our forecasts for key economic indicators and the policy interest rate.

- Following the Federal Reserve’s 25 basis-point rate hike on July 26 to a range of 5.25%–5.5%, a 22-year high, Chairman Jerome Powell emphasised that U.S. monetary policy hasn’t been restrictive enough for long enough, and that he didn’t anticipate that rate cuts would be plausible this year, a view that Vanguard shares. In this context, we believe the Fed’s policy rate target range could finish 2023 as high as 6%–6.25%.

- While the pace of inflation, based on the Personal Consumption Expenditures (PCE) index, continued to ease in June, we believe that stickier components including services other than shelter will challenge a sustainable path to 2%. We have increased our year-end 2023 forecasts to 3.2% for headline inflation and 3.6% for core inflation, which strips out volatile food and energy prices.

- We’ve lowered our year-end forecast for the unemployment rate to a below-consensus 3.8%, given the labour market’s continued robustness. We’re closely watching wage growth, which has reescalated modestly, calling into question the idea that wage growth will moderate without job losses.

- We’ve increased our forecast for 2023 GDP growth to 1.8% amid a pick-up in business investment, government spending, and housing activity. Recession in the next 18 months, however, remains our baseline view. “In essence, we’ve pushed out the timeline for a U.S. recession to 2024 as we’ve yet to feel the full effect of Fed interest rate tightening,” said Josh Hirt, a Vanguard senior economist.

China

The post-COVID-19 economic recovery that took hold in the first quarter of 2023 is being challenged from all sides. “The deceleration in economic activity in July was broad-based,” said Grant Feng, a Vanguard senior economist. “It reflects a deepening property slump, subdued investment demand, waning consumption, and weakened external sector momentum.”

- We recently lowered our forecast for full-year 2023 GDP growth from a range of 5.5%–6% to a range of 5.25%–5.75%, given a sharper-than-expected slowdown in the second quarter. The slow start to the third quarter intensifies downside risks to that forecast.

- Growth in retail sales, a key measure of consumption, slowed to 2.5% in July despite favorable comparisons to year-earlier numbers and was well below consensus. Industrial production grew by 3.7% year-on-year in July, slower than 4.4% growth in June.

- China’s economy fell into deflation in July, with broad consumer prices falling by 0.3% compared with a year earlier. That followed several months of price declines. We’ve lowered our full-year forecast for headline inflation to 0.5%–1.5%, down from our previous forecast of 1%–1.5%.

- The People’s Bank of China cut its policy rate by 0.15 percentage points to a record low of 2.5%. We foresee a further cut to the policy rate of 0.10 to 0.20 percentage-points, as well as further cuts to the reserve requirement ratio—the amount of cash that banks must keep in reserve.

- Vanguard doesn’t believe that such rate cuts will have a substantial impact on their own, given falling prices and apprehension around China’s growth outlook. “We anticipate a comprehensive and coordinated policy package on fiscal, monetary, and regulatory fronts, including accelerated government bond issuance, further policy rate cuts, relaxed restrictions to boost property demand, and regulatory easing for the private sector,” Feng said.

Euro area

The euro area didn’t fall into recession early this year after all, according to revised GDP figures showing that growth was flat in the first quarter. The narrative of economic weakness doesn’t change, however.

- High-frequency data suggest continued contraction in the manufacturing sector and sharply slowing momentum in the services sector in the third quarter.

- GDP grew by 0.3% in the second quarter, according to a second flash estimate. However, without Ireland’s typically volatile contribution and delivery of a cruise ship in France, euro area GDP would have grown only 0.1%. In our base case, we expect the economy to contract in the third and fourth quarters of 2023.

- Headline inflation slowed to 5.3% in July compared with a year earlier, according to a July 31 flash estimate by the European Union’s statistical agency. Energy prices are no longer contributing to headline inflation, having been its primary driver for much of 2022, but services inflation remains sticky. As the economy weakens, we expect the pace of inflation to decelerate in the second half of 2023, with core inflation ending the year around 3.3%.

- The European Central Bank (ECB) raised its deposit facility rate to 3.75% on July 27. We don’t rule out one more quarter-point hike and expect the rate to stay at its peak level through an anticipated recession to allow the effects of more restrictive policy to work their way through the economy. We don’t foresee ECB rate cuts until the second half of 2024 at the earliest.

- The unemployment rate remained steady in June, unchanged from a revised record low of 6.4% in May, but in this region as well we are skeptical that there could be a “painless disinflation” in which prices normalise without meaningful job losses. We expect the unemployment rate to rise as high as 7%.

United Kingdom

Recent inflation data emphasise the UK economy’s challenges. Continued strong inflationary pressures suggest that the Bank of England isn’t yet in position to halt the interest rate increases that began in December 2021 and now total more than 5 percentage points. We expect a rising policy rate to weaken demand and eventually weigh on the labour market.

- The pace of year-on-year headline inflation eased to 6.8% in July compared with a year earlier, but remained well above the central bank’s comfort level. Core inflation held steady at 6.9% year-on-year. Vanguard expects both measures to fall to close to 5% by the end of 2023, helped by comparisons with year-earlier prices for energy, food, and core goods. But we foresee limited progress on services inflation the rest of the year.

- The Bank of England raised the bank rate by 25 basis points to 5.25% and signaled that further monetary policy tightening would take place in the face of inflationary pressures. We continue to foresee one or two more rate increases, with no rate cuts until the second half of 2024 at the earliest.

- GDP growth surprised to the upside, posting an increase of 0.2% in the second quarter compared with the first. Private consumption grew more than expected in the quarter, and business investment grew, defying expectations for a modest contraction. In June, manufacturing and construction output were better than expected.

- The unemployment rate rose to 4.2% in the April–June period, up from 4.0% in the March–May period. Wage growth accelerated, with private sector pay (which excludes bonuses) up by 7.8% in the three months through June compared with a year earlier, the highest annual growth rate since comparable records began in 2001.

Emerging markets

Aggressive monetary policy tightening has taken hold in some emerging markets, bringing inflation down sufficiently to allow for the start of rate cuts. “We would expect emerging markets that raised rates the most to also cut them the most, though the path and timing of cuts could differ among nations and from trajectories when central banks were raising rates,” said Vytas Maciulis, a Vanguard economist.

- Leading indicators show that emerging markets remain resilient on aggregate. We have modestly boosted our year-end 2023 GDP forecast to 4%, but will be watching developments in China, given its strong GDP weight and the effect of its activity on other emerging markets.

- In Chile, inflation has fallen by more than 5 percentage points from its peak, which paved the way for a 1 percentage point cut in the central bank’s key interest rate to 10.25%.

- Inflation in Brazil has fallen by an even greater amount, permitting its central bank to cut its Selic rate to 13.25%.

- Inflation has decelerated more slowly in Mexico than in Brazil or Chile, by fewer than 2 percentage points from its recent high. The Bank of Mexico’s overnight interbank rate target remains 11.25% and we aren’t anticipating any cuts in 2023.

- Policy interest rates are modestly restrictive in emerging Asia, where inflation didn’t present the challenge that it did in Latin America. In much of emerging Europe, policy interest rates haven’t yet exceeded rates of inflation that largely remain higher than in Latin America or emerging Asia.

Canada

The Consumer Price Index accelerated from 2.8% year-on-year for June to 3.3% for July largely due to base effects for gasoline prices. The average of the Bank of Canada’s preferred core measures of inflation softened but remained above target. “The Bank of Canada will no doubt remain vigilant, but the inflation data gives it room to pause in September to further assess the impacts of its tightening thus far,” said Rhea Thomas, a Vanguard economist.

- Two recent rate hikes have put the BOC’s overnight rate target at 5.0%, and it may go higher should progress on inflation remain slow. The bank noted that increased immigration has contributed to rising consumer spending and housing demand, but that it could also help ease labour shortages and wage pressures.

- The labour market showed signs of softening in July, with the unemployment rate rising for the third straight month to 5.5%. Nearly 45,000 jobs were lost in construction; we’ll be watching in the next few months for how many of those jobs come back quickly given the impact that labour strikes and wildfires may have had on the sector.

- Wage pressures remained elevated. Wages were up 5% compared with a year earlier and were higher than the 4.2% year-over-year gain in June.

- First-quarter GDP growth of 3.1% on an annualised basis exceeded expectations, but we continue to foresee 2023 GDP growth of just less than 1% and a recession late in the year as the effects of higher interest rates spread through the economy.

Vanguard’s outlook for financial markets

Our 10-year annualised nominal return and volatility forecasts are shown below. They are based on the June 30, 2023, running of the Vanguard Capital Markets Model (VCMM). Equity returns reflect a 2-point range around the 50th percentile of the distribution of probable outcomes. Fixed income returns reflect a 1-point range around the 50th percentile. More extreme returns are possible.

Australian equities: 4.2%–6.2% (21.7% median volatility)

Global ex-Australia equities (unhedged): 4.8%–6.8% (19.4%)

Australian aggregate bonds: 3.8%–4.8% (5.5%)

Global bonds ex-Australia (hedged): 4.0%–5.0% (4.7%

Notes

All investing is subject to risk, including the possible loss of the money you invest.

Investments in bonds are subject to interest rate, credit, and inflation risk.

Investments in stocks and bonds issued by non-U.S. companies are subject to risks including country/regional risk and currency risk. These risks are especially high in emerging markets.

Important

The projections and other information generated by the Vanguard Capital Markets Model (VCMM) regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time.

The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model is a proprietary financial simulation tool developed and maintained by Vanguard’s primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include U.S. and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, U.S. money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

General advice warning

This article contains certain 'forward looking' statements. Forward looking statements, opinions and estimates provided in this article are based on assumptions and contingencies which are subject to change without notice, as are statements about market and industry trends, which are based on interpretations of current market conditions. Forward-looking statements including projections, indications or guidance on future earnings or financial position and estimates are provided as a general guide only and should not be relied upon as an indication or guarantee of future performance. There can be no assurance that actual outcomes will not differ materially from these statements. To the full extent permitted by law, Vanguard Investments Australia Ltd (ABN 72 072 881 086 AFSL 227263) and its directors, officers, employees, advisers, agents and intermediaries disclaim any obligation or undertaking to release any updates or revisions to the information to reflect any change in expectations or assumptions.

Vanguard

August 2023

vanguard.com.au

vanguard.com.au