Don't ever do a Budget again on the back of an envelope or using anything hand written. Via this site's financial tools, secure client portal or calculators you and your family excellent online help AND all information is kept for re-use over and over again. Don't spend time doing the same thing again and again, do the hack work online once and you only have to adjust data from then on. Great for your kids as well.

These tools are an added service to help you, our clients, gain more from the what we provide.

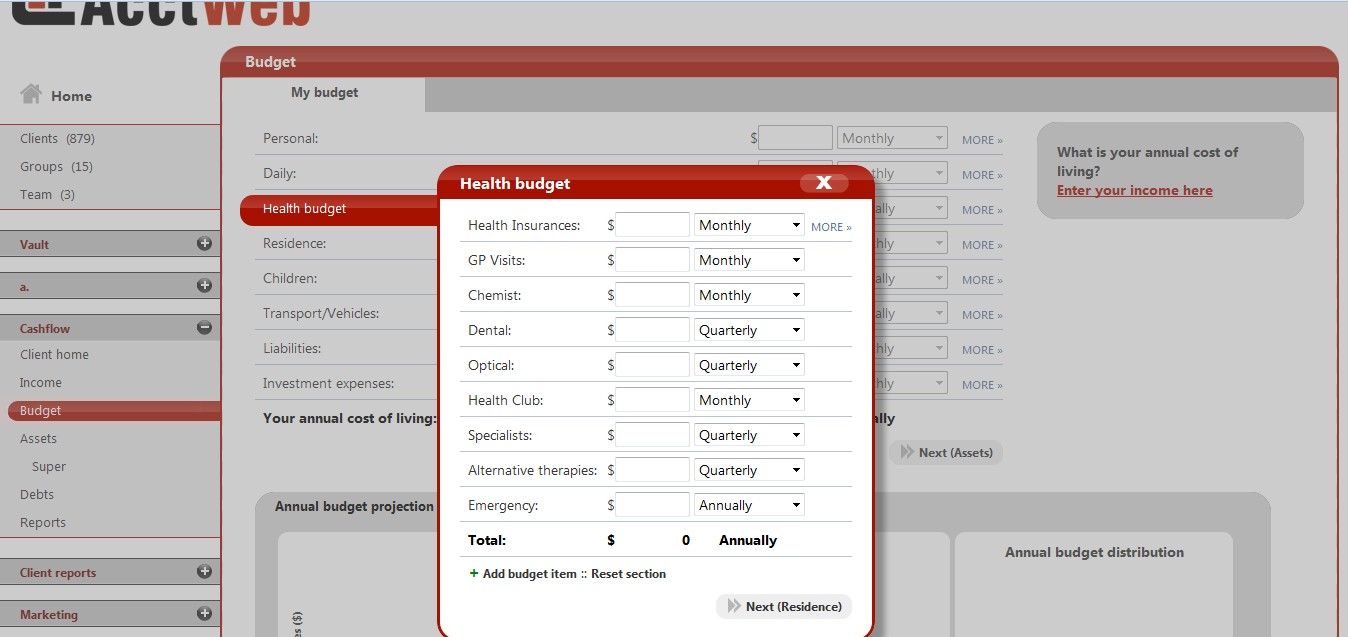

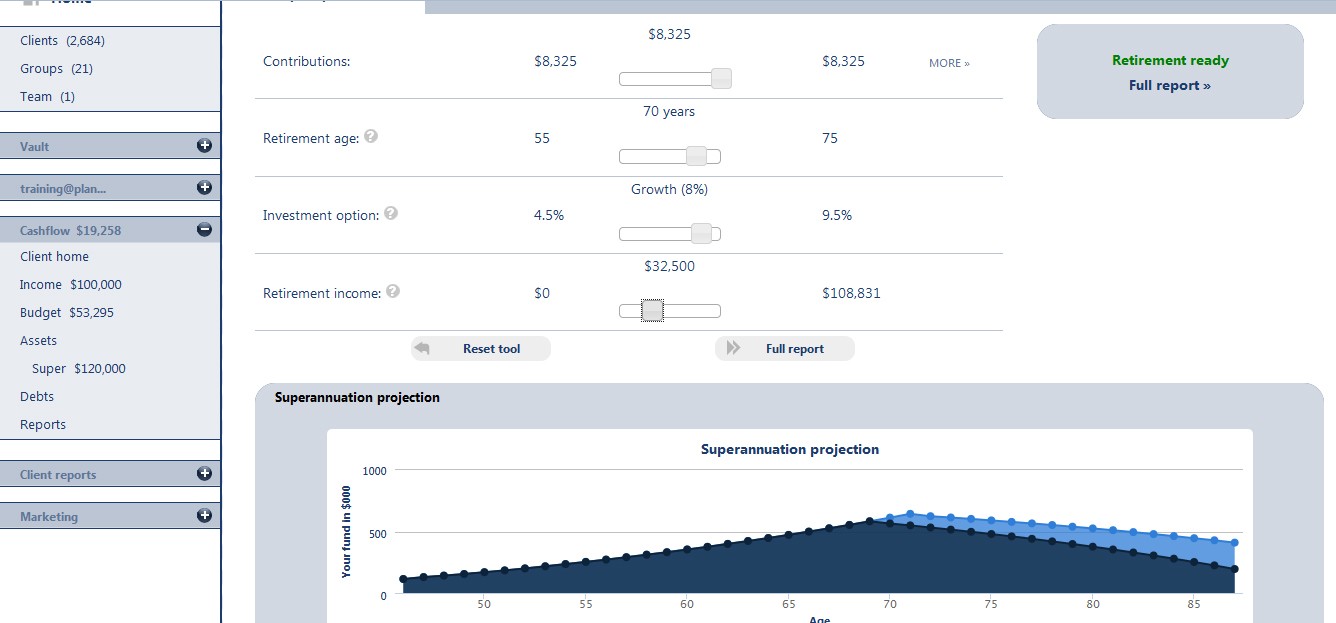

You may think that working on a Budget or cash flow isn’t your cup of tea but when things are tight or you need to look long term there is no better way to manage how your money is used. 24/7 access and if you have a question you don't have far to go to ask.

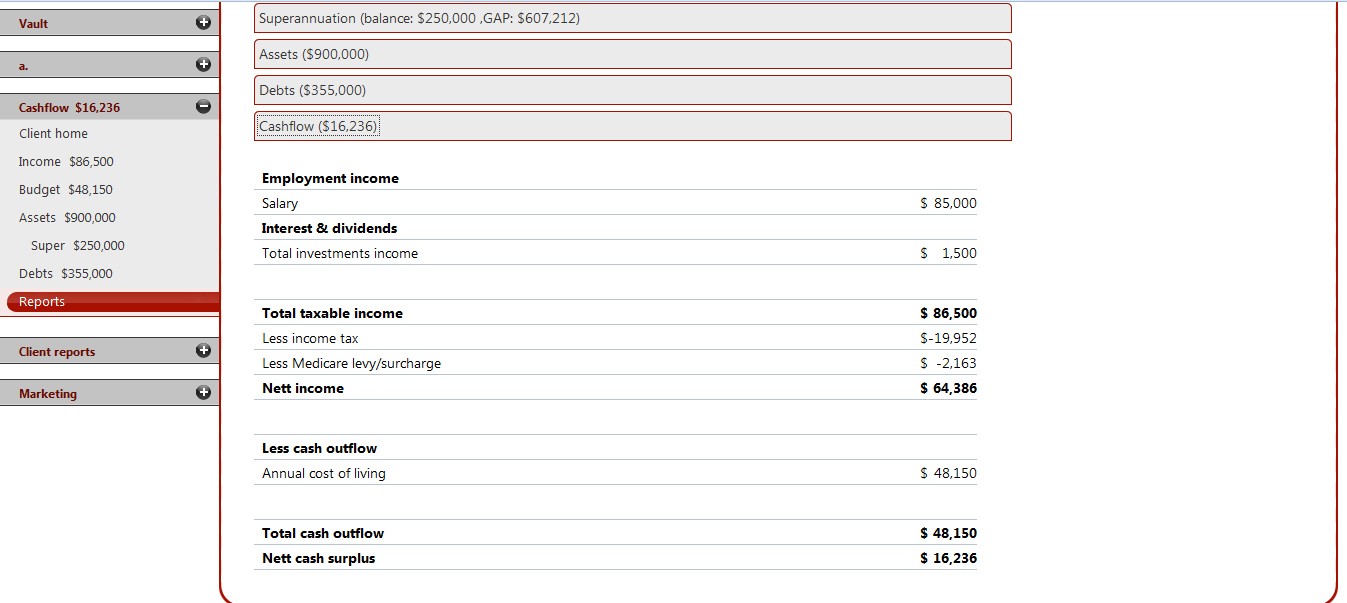

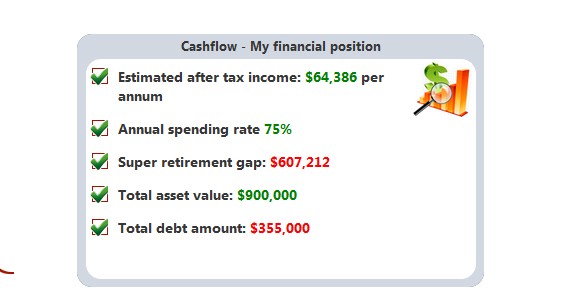

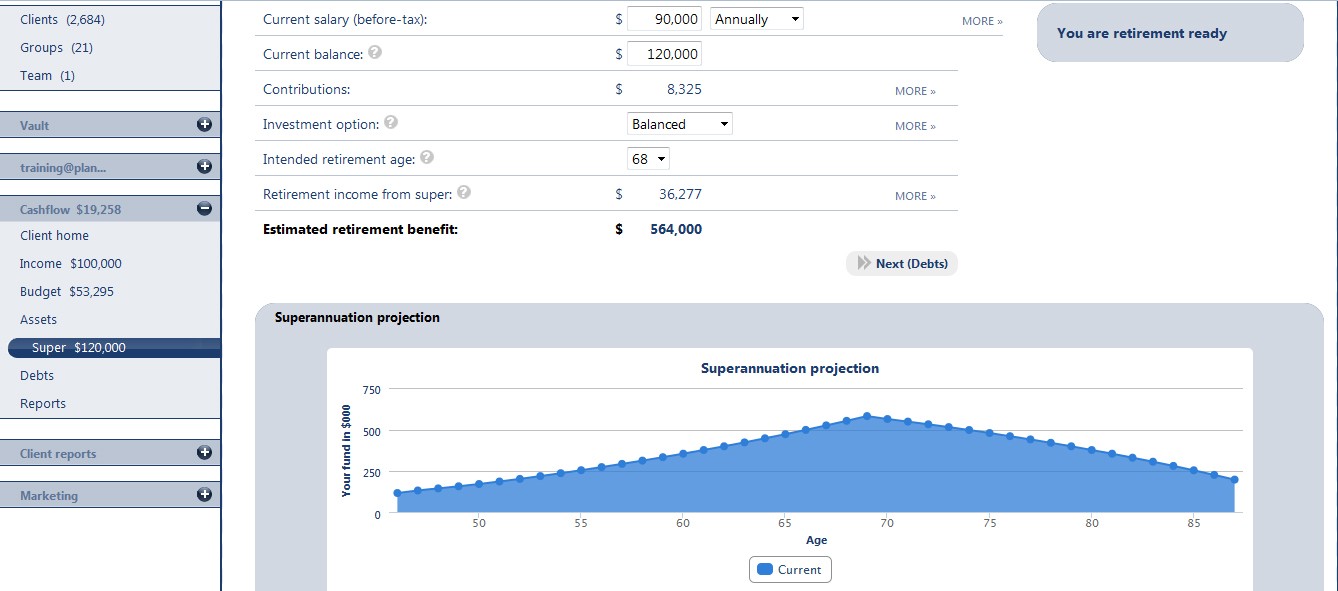

The following images are examples of what can be done, also there is a longer article about overall financial literacy following the first few points.

When you feel the urge then a quick trip to our website is a good thing to do, it has all the tools you need and more. Also any information you add that’s relevant to other tools is automatically transferred saving you time and effort.

Give it a go. Start with a Budget or cash flow analysis or Super scenario. It may take a bit of time but even a few minutes here and there is good and everything you add will be waiting until the next time you log in.

---------------------------------------

Cracking the money code

Literacy is the key that unlocks a world of knowledge. In the investment world financial literacy is how investors can crack the code of our sophisticated and at times complex world of money.

The issue of financial literacy is both broad and multi-layered. At one end of the spectrum there are those people who are effectively shut out of the modern financial system because their lack of financial literacy means they cannot access even the most basic of financial products.

The National Australia Bank first commissioned research by the Centre for Social Impact back in 2011 and recently updated the work in June 2013. It defines financial exclusion where individuals lack access to appropriate and affordable financial products such as transaction accounts, general insurance and a moderate amount of credit.

The research found that about 17 per cent of the adult population in Australia are either fully or severely excluded from financial services. A big concern is that the figure is rising not falling.

Improving financial literacy is a significant challenge and there are a range of initiatives underway including getting basic money management skills embedded in the school curriculum nationally.

ASIC has responsibility for implementing a national financial literacy strategy and a strong focus of that strategy is looking at improving educational pathways and content.

That is to be applauded but clearly this is an issue that ranges from the basic - understanding mobile phone contracts, credit card debts and household budgeting - right on up to more sophisticated challenges like understanding your superannuation.

As our superannuation system continues to grow and mature it is likely to have an ever-increasing role in educating Australians around long-term savings and planning for their retirement.

Australia's superannuation system is world-class in terms of a system structured to build retirement savings. But one of its core strengths - the mandatory nature of contributions from salaries - brings with it the issue of lack of member engagement because the majority of fund members do not actively make decisions either about the fund or the investment approach.

By its design there is a paternalistic side to our super system that works in a behavioral sense against fund members being fully engaged with their super account in the same way that they are with their banking or credit card accounts.

Ask yourself - or friends/work colleagues - when was the last time you checked your super fund balance?

The other factor working against super is its long-term nature - it is not hard to put off doing something when you can't get your hands on the money for 30 years.

Financial literacy is an essential life skill if people are to function and succeed in the modern world. Education and banking services are clearly on the front line of improving financial literacy, but increasingly there must be a role for super funds because they are going to be much more integral in people's lives as the system grows and the population ages.

By Robin Bowerman

Smart Investing

Principal & Head of Retail, Vanguard Investments Australia

17th-September-2016 |