.

Specific points in time can be useful for investors, although they’re generally less relevant over the long term.

Take the end of the 2022-23 financial year on Friday 30 June for example. It marked the end of a 12-month period during which fears about deteriorating economic conditions spurred ongoing volatility on global investment markets.

It was a similar story a year earlier at the end of the 2021-22 year as markets volatility led to negative investment returns across most asset classes, from shares to bonds.

Yet, despite the persistent volatility, 30 June 2023 marked a sharp turnaround in investment returns from the end of the previous financial year.

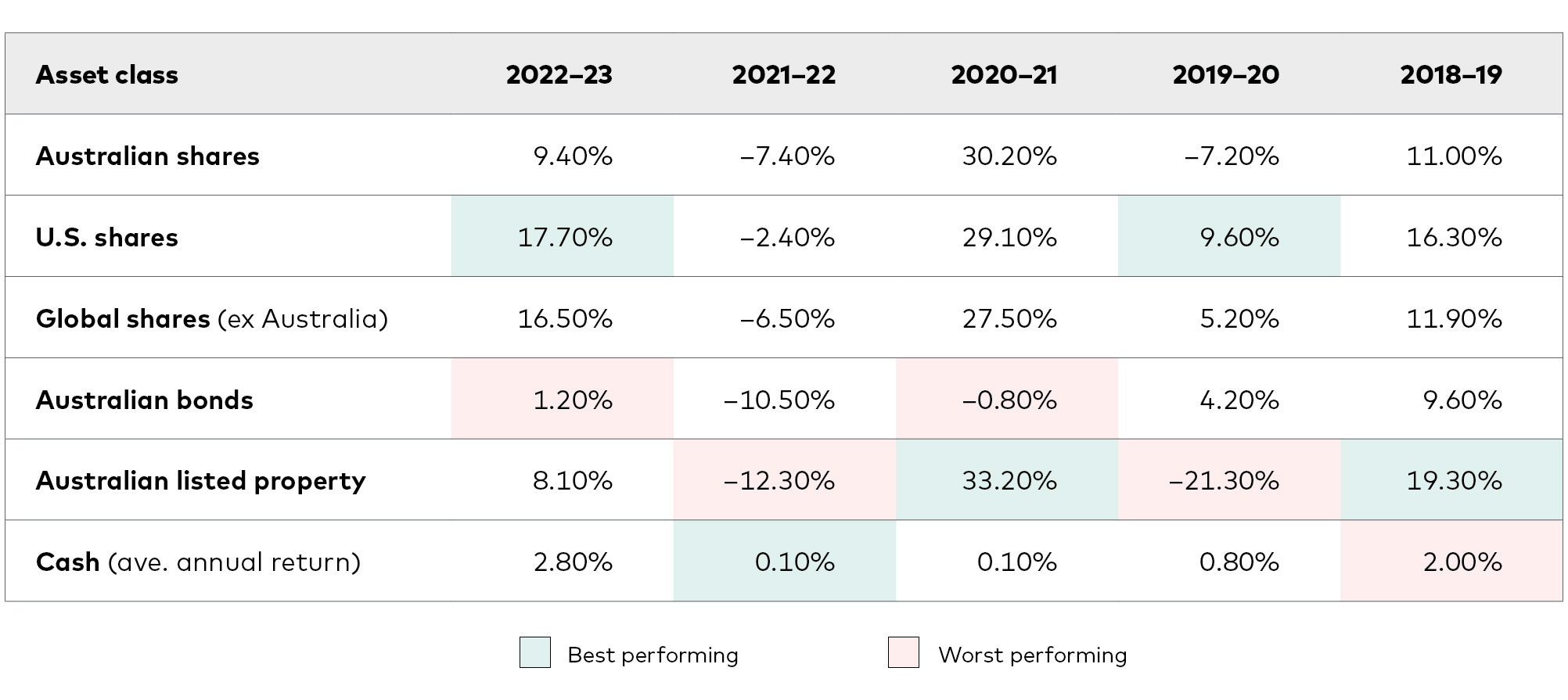

After falling more than 10% in 2021-22, the Australian share market as measured by the S&P/ASX 300 Index (which tracks the share prices of the 300 biggest companies listed on the Australian Securities Exchange) regained almost all of its lost ground.

From 1 July 2022 to 30 June 2023 the S&P/ASX 300 Index rose by just under 9.4%.

It was an even stronger 12-month period for investors on the United States share markets. The S&P 500 Index, which tracks the top 500 companies there, fell more than 11% in 2021-22. But between 1 July 2022 and 30 June 2023 it completely erased that loss by rebounding around 17.7%.

Meanwhile, after recording a fall of more than 10% in financial year 2021-22, the Australian fixed interest (bond) market – measured by the Bloomberg AusBond Composite 0+ Year Index – ended the 2022-23 financial year with a positive return of more than 1.2%.

That sharp turnaround in nominal, non-inflation-adjusted, terms largely reflects the impact of rising interest rates, which fuelled strong investor inflows into Australian and international bonds.

Just a line in the sand

The end of each financial year is relevant to many Australian investors from a taxation perspective.

Income distributions such as share dividends and bond coupon payments received over the period generally need to be recorded and declared by taxpayers for tax purposes.

Likewise, taxpayers generally need to record all their buy and sell transactions made during the financial year to track net capital gains and losses, also for tax purposes.

However, aside from the requirement to complete and lodge an income tax return with the Tax Office after 30 June each financial year, the crossover from one financial year to the next is merely just a line in the sand. Trading on investment markets will always resume on the first business day of a new financial year, typically changing all the market returns that were recorded as at the close of business at the end of the previous financial year.

Five financial years of returns

Sources: S&P/ASX 300 Index (Australian shares); S&P 500 Index (U.S. shares); MSCI World ex-Australia Net Total Return Index (Global shares ex Aust); Bloomberg AusBond Composite 0+ Year Index (Australian bonds); S&P/ASX 200 A-REIT Total Return Index (Australian listed property); Reserve Bank of Australia's Official Cash Rate (Cash).

Out of all of the asset classes listed above, in 2022-23 the U.S. share market produced the highest return, followed by global shares excluding Australia. In the previous financial year cash was the only asset class listed to deliver a positive return – albeit that after inflation, the purchasing power of cash savings declined.

High inflation levels are continuing to erode cash returns, and over the long term cash has produced the lowest return of all major asset classes.

The bottom line

When deciding where to invest, it’s important to understand that the best and worst performing asset classes will often vary year to year.

Successful investing often benefits from having a good balance of asset classes.

Rather than trying to pick the winning investment each year, spreading your investments across a wide range of assets may help to reduce the risk of loss over longer periods that could occur if you had all your capital tied to just one asset class.

Investors who are well diversified tend to enjoy a smoother investment ride over the long term.

Long-term returns data also suggests that time in the market will deliver consistent growth over longer periods despite periods of short-term volatility.

Tony Kaye, Senior Personal Finance Writer

vanguard.com.au

13th-August-2023 |