Key points

- 2020-21 saw investment returns rebound after the coronavirus hit depressed 2019-20 returns.

- Key lessons for investors from 2020-21 were to: allow that share markets look ahead; timing markets is hard; don’t fight central banks; and turn down the noise.

- Over the next 12 months returns from a well-diversified portfolio are likely to be slower but still solid.

Introduction

The past financial year saw a spectacular rebound in returns for investors as the focus shifted from the recession to recovery against a backdrop of policy stimulus and vaccines. This note reviews the last financial year and takes a look at the outlook.

The big developments of the last financial year

A year ago, many were wondering whether share markets had gone bonkers as they pushed higher despite lots of bad news. To be sure there were big negatives over the last 12 months:

- The global and Australian economies were confirmed to have seen deep recessions in first half 2020.

- There have been several waves of coronavirus globally, propelled over the last six months by new and more virulent strains. This in turn drove numerous returns to lockdowns.

- Budget deficits and public debt relative to GDP blew out in many countries to levels not seen since the end of WW2.

- The US saw a divisive election that turned violent with an invasion of the Capitol by Trump supporters.

- Tensions between Australia and other Western democracies with China have increased with more talk of a cold war.

- Bond yields rose sharply early this year on inflation fears & talk of an early exit from easy money, notably by the Fed.

However, for investors in well diversified portfolios the bad news was dominated by the good, in particular:

- Despite various coronavirus-related setbacks, global growth has seen an almost Deep V rebound and is on track for 6% growth this year and 4% next, after last year’s 3% slump.

- Australian GDP has rebounded faster than expected to be one of the few developed countries to see GDP back above pre-coronavirus levels, despite numerous snap lockdowns - this in turn has driven a sharp rebound in company profits.

- Good news on vaccines and their deployment in developed countries has provided confidence in continued recovery.

- This has been reinforced by key central banks - notably the Fed and RBA - shifting to focus on actual inflation being sustained at target before tightening.

- The election of Joe Biden in the US has reduced global policy uncertainty and led to much more US fiscal stimulus.

- Australian fiscal stimulus continued, dulling any “fiscal cliff”.

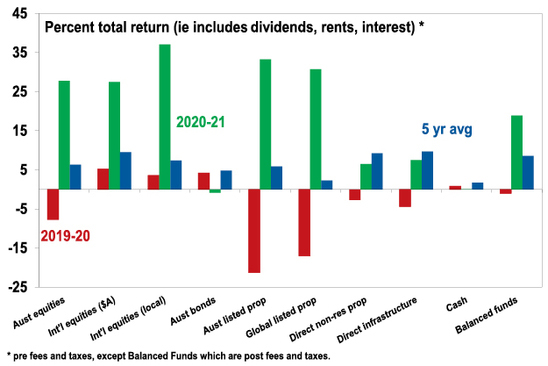

Strong returns more than making up for a poor 2019-20

With the recession and profit slump associated with coronavirus already factored in and giving way to recovery, and vaccines and stimulus providing confidence it would continue, the past financial year has been very strong for growth assets.

Global shares returned 37% in local currency terms. A rebound in the growth sensitive Australian dollar saw this reduced to a still very strong 28% in Australian dollar terms.

Australian shares returned 28% helped by a sharper rebound in the Australian economy, a surge in profits and numerous companies reinstating or increasing their dividends. Of course, this followed a 7.7% loss the previous financial year.

Reflecting the growth rebound, listed property rebounded and unlisted property and infrastructure also saw a good recovery.

Of course, bonds performed poorly as bond yields rose and cash had a near zero return reflecting the near zero cash rate.

This drove very strong returns from balanced growth super funds of around 19% after fees and taxes. Over the last five years super fund returns averaged around 8.5% pa which is not bad given sub 2% bank deposit rates and inflation.

2020-21 - major asset class returns

Source: Thomson Reuters, AMP Capital

Australian residential property prices also surged on the back of ultra-low rates, various incentives and economic recovery resulting in their strongest 12-month gain since 2004.

Key lessons for investors from the last financial year

- Share markets look ahead – and they climbed a wall of worry of the last year, but this is what they always do.

- Timing markets is hard – staying fully invested as markets rebounded despite the recession and ongoing coronavirus scares would have been very hard at times.

- Don’t fight the Fed or the RBA – despite zero interest rates they still impact investment markets in a big way.

- Investment valuations need to be assessed relative to interest rates – low rates mean higher PEs.

- Turn down the noise – the noise around investing is now at fever pitch making it very hard to stay focused on long term investing, so the best thing is to turn it down.

The worry list weighing on the outlook

Share markets have had strong gains from last year’s lows (US shares are up 94%, global shares are up 83% and Australian shares are up 60%) and are no longer unambiguously cheap so the easy gains are likely behind us. And as always there remains a worry list to contend with.

- First, coronavirus is continuing to cause havoc with the global trend in new daily cases starting to head up again, particularly driven by the newer more transmissible Delta and Beta variants. This is particularly evident in lowly vaccinated countries – like parts of Asia, Africa and South America. And in Australia, albeit the numbers are very low. But it’s also evident in advanced more vaccinated countries like the UK, parts of Europe and the US.

- Second, inflationary pressures have increased globally with reopening and this is most evident in the US.

- Third, at the same time central banks are starting to back away from ultra-easy monetary policy, eg, the Fed dots flagging an earlier start to rate hikes than previously and the RBA starting to taper its bond buying from September.

- Fourth, peak fiscal stimulus has likely already been seen.

- And geopolitical tensions between Western democracies and China are arguably continuing.

The positives are likely to ultimately dominate

These negatives have the potential to cause a correction in share markets. However, there are a bunch of positives that are ultimately likely to dominate in terms of investment markets.

- First, while coronavirus cases may be on the rise again the vaccines are keeping a light shining at the end of the tunnel. They don’t appear to be completely effective against getting infected by the new variants, but the evidence suggests they are 90%+ effective in preventing serious illness requiring hospitalisation and causing death. In the countries that are further advanced in vaccination (eg, Israel, the UK, most of the US, Europe, etc.) this should allow reopening to continue without rising new cases overwhelming the hospital system, ie, learning to live with coronavirus. For those countries further behind in reaching herd immunity – like Australia – it likely means a continuing reliance on snap lockdowns to keep case numbers down and head off bigger outbreaks that overwhelm the hospital system and send economies backwards. But the evidence so far is that snap lockdowns don’t derail the recovery. And global production schedules point to plenty of vaccines being available later this year enabling Australia and other vaccine laggards to proceed down the same path as other advanced countries later this year or early next in terms of avoiding lockdowns.

- Second, while inflation pressures have picked up this is mainly evident in the US and largely reflects pandemic related distortions. Other countries including Europe, Japan and Australia are seeing far less of an inflation spike.

- Third, this in turn will likely keep central banks gradual in removing ultra-easy monetary policy with rates likely to remain low for a long while yet. We don’t expect the first rate hikes in the US and Australia till 2023 (and Europe and Japan are a long way behind that) and even then it will take several years to reach tight monetary policy that threatens economic activity and company profits.

- Fourth, against this backdrop while we have probably seen the peak in terms of growth momentum globally, the recovery is likely to continue as the rollout of vaccines progressively allows more countries to safely reopen, pent up demand is spent (evident in about $US2.5trn of excess savings in the US and about $200bn in Australia) and monetary policy remains very easy.

Global Composite PMI vs World GDP

Source: Bloomberg, AMP Capital

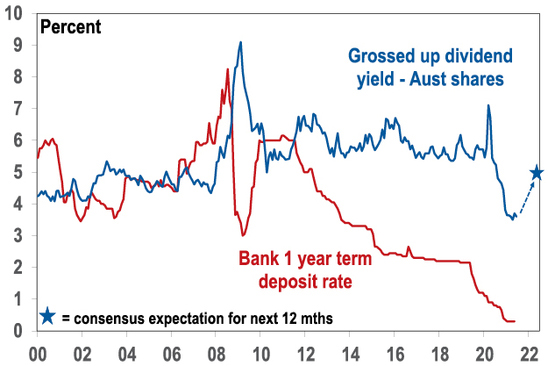

- Finally, while traditional valuation measures for shares show them to be expensive, they continue to look okay relative to still low bond yields. This is particularly evident in Australia with a grossed-up dividend yield of 5% or so for the year ahead well above bank term deposit rates of around 0.5%.

Aust shares offer a very attractive yield versus bank deposits

Source: RBA; AMP Capital

What about the return outlook?

While there is a risk of a short-term correction in shares and returns are likely to slow from the pace of the last year, overall returns from well diversified portfolios are still likely to be reasonable over the next 12 months.

- Shares are expected to see okay returns helped by strong economic and earnings growth and still low interest rates.

- Cash and bank deposit returns are likely to remain poor as the RBA is expected to keep the cash rate at 0.1%.

- Low starting point yields and a capital loss from gradually rising yields are likely to result in low returns from bonds.

- Unlisted commercial property may still see some weakness in retail and office returns but industrial is likely to be strong. Unlisted infrastructure is expected to be solid.

- Home prices are expected to rise 20% this year but slow to 5% next year as poor affordability, rising fixed rates, tighter lending standards and reduced population growth impact.

- The $A is likely to trend up in line with global recovery and strong commodity prices.

Things to keep an eye on

The key things to keep an eye on are: covid hospitalisations and deaths in more vaccinated countries; inflation; central banks; growth momentum; and tensions with China.

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

|