Key points

- The absence of significant macro policy differences between the new Labor Government and the Coalition suggests minimal impact on the share market & the $A.

- There could be some short-term uncertainty if Labor has to rely on minority parties or independents, but its looking like Labor will be able to govern in its own right.

- The key economic challenges for the new Government relate to inflation, interest rates & housing affordability. Higher inflation & rates argue for faster deficit reduction.

Australia has a new government

The ALP won the election and is set to Govern most likely in its in own right or as a minority government. Following its loss in the 2019 election which was partly blamed on a “radical” tax & spend agenda, the ALP adopted a “small target” approach this time, so its economic policies are not significantly different to those of the outgoing Coalition Government. However, there are still some areas of difference and uncertainty. This note looks at what is expected in terms of policies and implications for the budget, economy & investment markets.

Policy changes

Based on their election platform, key economic policy changes under the Labor Government will include the following:

- Faster climate action with a 43% cut to emissions below 2005 levels by 2030 versus the Coalition’s 26-28% cut. This could be increased under pressure from Greens and “teals”.

- This includes investing $20bn in electricity infrastructure and boosting renewables to 82% of electricity by 2030.

- An extra $2.5bn per annum in aged care funding.

- An extra $750m on Medicare.

- Raise the childcare subsidy to 90% for the first child in care.

- Create 20,000 more university places & free TAFE places.

- Support for manufacturing with a $15bn National Reconstruction Fund and Federal procurement programs.

- Housing support policies with: a $10bn Housing Australia Fund to build 30,000 social homes over five years; a Help to Buy scheme with the Government to take up to 40% equity in up to 10,000 first home buyer home purchases a year; support for the Coalitions 50,000 low deposit purchase scheme with an additional 10,000 places in regions; support for the Coalition’s super concessions for downsizers over the age of 55; and the establishment of a National Housing Supply and Affordability Council to help boost supply.

- Encourage the Fair Work Commission to raise the Minimum Wage by 5.1%. This would normally flow through to 2.6m workers on awards and raise concerns about a wage price spiral, but PM Anthony Albanese has suggested it would only cover those on the minimum wage which is 180,000.

- Make gender pay equity an objective in the Fair Work Act.

- The ALP proposed no tax hikes apart from measures to tax multinationals more. But it’s not committing to the 23.9% Coalition cap on the tax to GDP share and wants to shift the focus to the “quality” of spending, suggesting a somewhat higher tax and spending share of GDP over the long term.

- Implement the Uluru Statement from the Heart in full.

Impact on the budget and overall fiscal policy

Like the Coalition the ALP is largely looking to repair the budget by growing the economy rather than austerity. The new Government’s pre-election costings suggest extra spending of $18.9bn over the next four years offset by $11.5bn in saving to be from taxes on multinationals, a crackdown on tax avoidance and a cut in public sector spending. This will add an extra $1.9bn pa to the deficit. The table below compares the Coalition Government’s budget deficit projections for the next four years with the deficit under Labor’s policies. The ALP is also talking of $52bn in “off budget” funds (eg, the Housing Australia Fund) which will add to gross debt. The addition to the deficit is only 0.1% of GDP pa though and it should also be noted that if the improvement in the budget numbers since March due to higher commodity prices and lower unemployment continues then the deficit numbers could be much lower. Prior to the election the new Treasurer said he would give a statement updating the outlook in June and a new budget in October.

Budget deficit projections

Source: Federal Treasury Pre-Election Economic and Fiscal Outlook, ALP, AMP

Assessment and challenges

At a fiscal policy level, the differences versus the Coalition are trivial. The new Government looks inclined to allow a higher spending and tax share of GDP but note that the spending share is already projected at record levels under the Coalition. However, Labor faces big challenges in an era of higher inflation & interest rates and in relation to housing affordability.

The pivot in the economy to higher inflation poses a big challenge to the complacency around the budget deficit, much as the changed environment made life tough for the Whitlam Government in the 1970s. The days of low inflation and low bond yields allowing big budget deficits and high debt are likely behind us. This argues for a faster reduction in government borrowing (whether its “on” or “off budget”) to take pressure off inflation and interest rates and for more policies to boost productivity. And while new Treasurer Jim Chalmers has indicated a preparedness to undertake “budget repair” via a spending audit, this may not be enough if the fast-growing health and social services areas are protected. This in turn could see a return to some of the proposed 2019 tax hikes.

And without productivity enhancing reforms it’s doubtful that the 1.5%pa productivity growth assumption underpinning the March Budget can be achieved, which would mean waning growth in living standards and higher inflation. It also makes it harder for the Government to encourage higher wages without risking a wage price/spiral. Labor policies to boost childcare and use of lower cost sustainable energy will likely help in this regard but in the absence of significant tax, industrial relations, education and competition reforms it’s doubtful they will be enough.

As with the Coalition’s policies the new Government’s housing policies are more focussed on boosting demand – notably the expansion of low deposit schemes and the Help to Buy Scheme – which will result in higher than otherwise home prices. However, the construction of 30,000 social homes combined with the National Housing Supply and Affordability Council if appropriately focussed on boosting supply have the potential to help improve housing affordability. Its marginal though. The main impact on home prices will likely from come rising interest rates (which would have occurred whoever won the election) which we see driving prices down by 10-15% over the next 18 months and may prove to be a headwind for prices thereafter.

Shares, the $A, elections & political parties historically

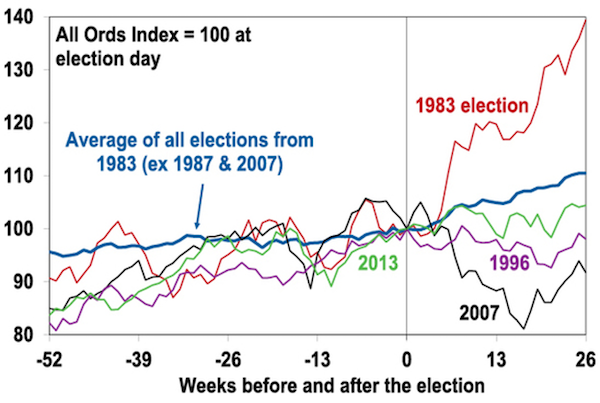

Since the 1980s there has been a tendency for Australian shares to rise after elections, as uncertainty is removed.

Australian equity market around election days

Source: Reuters, AMP

The next table shows that 3 months after the last 14 elections the share market saw an average gain of 4.5%.

Based on All Ords index. Source: Bloomberg, AMP

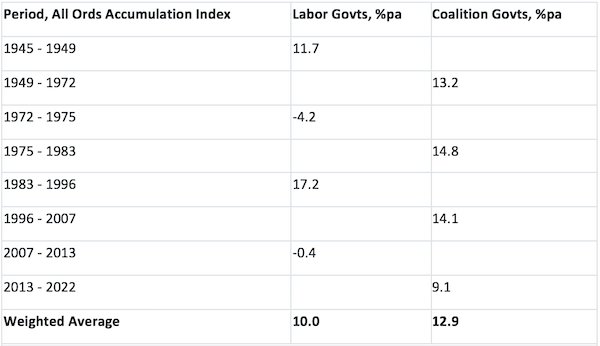

Since WW2 Australian shares have performed better under Coalition Governments, although the Whitlam and Rudd/Gillard Governments had the misfortune of severe global bear markets and the reformist Hawke/Keating period saw the strongest returns of any post war government.

Average share market returns of post war government

Source: ASX, Reuters, Bloomberg, AMP

For the Australian dollar since 1983 the average post-election response has been sideways to down slightly, but nothing to get excited about.

Implications for investment markets this time around

Labor’s macro policies not being significantly different from the Coalition’s and its victory not being a surprise suggests that the market reaction to the new Government will be minor and that investment markets will quickly move on to other things. So far that seems to be the case. With the share market down 3.5% over the last 8 weeks there is potential for a rebound ahead as political uncertainty is reduced but the Australian share market remains vulnerable to ongoing global concerns about inflation, interest rates and recession and these will likely dominate.

Industry sectors likely to benefit from the change in Government include clean energy, health, education, home builders & manufacturing, whereas heavy carbon emitters may lose.

While its now looking like Labor will be able to govern in its own right, the main risk for markets may come if that proves not to be the case and it has to rely on the Greens to form Government and they push the new Government down a far less business-friendly path, such as implementation of the Greens’ proposed super profits tax. However, even if Labor doesn’t secure a majority there will be plenty of “teal” independents in Parliament whose policies on climate, integrity and health align closely with Labor and for whom Labor should be able to gain support from. Labor’s (and the “teals”) desire to be more than a one term wonder should work against the new Government moving too far to the left on economic policies.

The change in Government has no implications on our growth, inflation and interest rate forecasts for this year. We continue to see the RBA raising the cash rate at is June meeting by 0.4% and increasing it to 1.5-2% by year end.

Concluding comment

Following the election there will no doubt be lots more political analysis, particularly in relation to the driving out of moderates from the LNP pushing it to the right & threatening the Coalition. More broadly, it seems that the election result represented a rejection of more right-wing/conservative views on climate, gender equity, health and integrity in support for what one of the new “teal” independent House of Reps members refers to as the “sensible centre”. Just as the 2019 election result represented a rejection of more left-wing tax and spend policies in favour of the “sensible centre”. In this sense it may be seen as a good thing for sensible centrist policy making in Australia.

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

|